You’ve probably had this thought at 11pm, staring at Zillow listings:

“Should I just buy a house already or am I being stupid with my money?“

Everyone has an opinion. Your parents say buy. Your coworker says the market is still too high. Your landlord just raised your rent again.

Here’s the truth nobody tells you: there’s no universally right answer. But there IS a right answer for your specific situation and by the end of this guide, you’ll know exactly what it is.

Let’s get into it.

Wisconsin Housing Market 2026 (Home Prices, Rent & Mortgage Rates)

Before you make any decision, you need to know what you’re walking into.

The Wisconsin housing market in 2026 is… complicated. Home prices haven’t crashed like some people predicted. But they haven’t become affordable overnight either.

Here’s the current reality:

Median home prices by city:

- Madison: $380,000–$420,000

- Milwaukee: $220,000–$270,000

- Green Bay: $210,000–$250,000

- Appleton: $240,000–$280,000

- Eau Claire: $195,000–$235,000

Mortgage rates are sitting at 6.5%–7% on a 30-year fixed. That’s not 2020 rates but it’s also not catastrophic if you plan smart.

Rental prices? Also up. A decent 2-bedroom in Wisconsin now runs:

- Madison: $1,500–$1,800/month

- Milwaukee: $1,100–$1,400/month

- Green Bay: $950–$1,200/month

- Smaller cities: $850–$1,100/month

Bottom line: Both options cost more than they did 3 years ago. Which is exactly why this decision matters more than ever in 2026.

How Much It Really Costs to Buy a House in Wisconsin (2026 Breakdown)

Most people calculate their mortgage payment and call it a day. That’s how people get financially blindsided 6 months after closing.

Let’s take a real example a $280,000 home in Milwaukee with 10% down:

One-time upfront costs:

- Down payment (10%): $28,000

- Closing costs (3%): $8,400

- Moving + immediate repairs: $3,000–$5,000

- Total you need saved: $40,000–$45,000 minimum

Monthly ongoing costs:

- Mortgage payment (6.75%, 30yr): $1,632

- Property taxes (~1.73% avg): $404

- Home insurance: $120

- Maintenance budget (1%/yr): $233

- Realistic total: ~$2,389/month

That maintenance line is what kills most first-time buyers. Furnace dies? $4,000. Roof needs work? $8,000–$15,000. Water heater? $1,200. These aren’t maybes they’re eventually-certainties.

The True Cost of Renting in Wisconsin (Is It Really “Throwing Money Away”?)

Renting gets called “throwing money away” but that’s lazy thinking.

Yes, you don’t build equity. But you also don’t pay for a broken furnace at 2am. You don’t lose $15,000 in closing costs if you need to move in 2 years. And your $40,000 that would’ve been a down payment? It can sit in a high-yield savings account earning 4–5% interest.

What renting actually buys you:

- Zero maintenance headaches

- Freedom to move for a better job or life change

- Predictable monthly expenses

- Liquidity your money stays accessible

Is it “throwing money away?” Only if you’re ignoring everything you get in return.

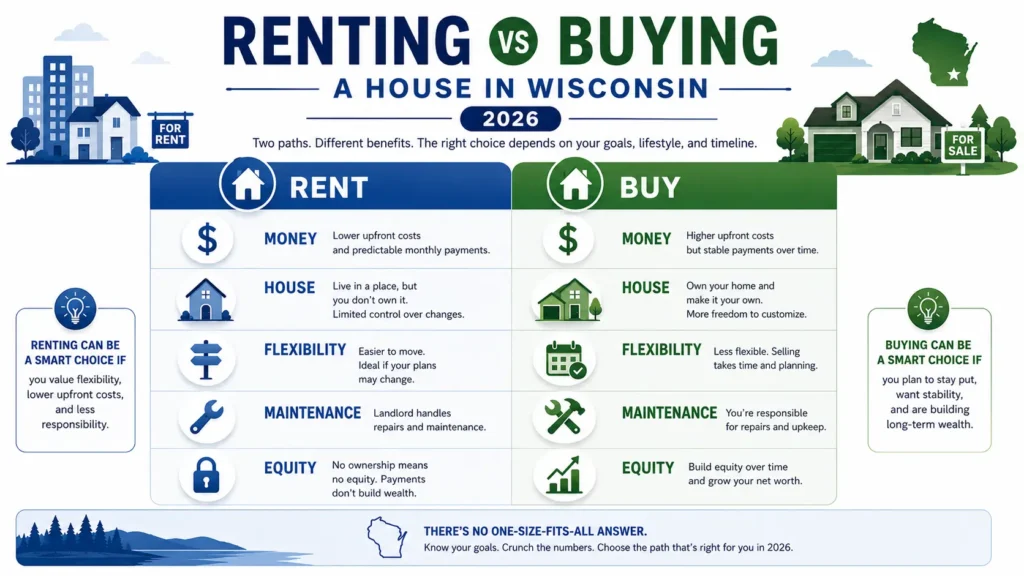

Renting vs Buying in Wisconsin: Side-by-Side Comparison

(Milwaukee example, $280,000 home vs comparable rental)

Buying:

- Upfront needed: ~$42,000

- Monthly cost: ~$2,389

- Flexibility: Low

- Builds equity: Yes

- Maintenance risk: Your problem

Renting:

- Upfront needed: ~$2,600 (deposit)

- Monthly cost: ~$1,300

- Flexibility: High

- Builds equity: No

- Maintenance risk: Landlord’s problem

Monthly difference: ~$1,089 more to own

That $1,089/month gap is the key number. The question is what do you get for paying it?

Over 7 years of ownership, you’d build roughly $40,000–$60,000 in equity (through payments + appreciation). You’d also have stability, a place you can actually customize, and protection against rent increases. But only if you stay long enough.

The Break-Even Point in Wisconsin (5–7 Year Rule Explained)

Here’s what nobody talks about in the rent vs buy debate:

Buying a home in Wisconsin costs you money for the first few years even if prices go up.

Why? Closing costs, transaction fees, early mortgage payments (which are mostly interest, not equity) all eat into your gains early on.

In Wisconsin’s current market, the typical break-even point is 5–7 years.

What this means practically:

- Staying less than 5 years → Renting almost always wins financially

- Staying 5–7 years → It’s roughly a toss-up depending on appreciation

- Staying 7+ years → Buying almost always wins financially

This single factor how long you’ll stay matters more than interest rates, home prices, or anything else.

Should You Buy a House in Wisconsin? (5 Key Questions to Ask)

Before you call a realtor or fill out a rental application, answer these honestly:

1. How long will you stay?

If the answer is “I’m not sure” that alone is reason to keep renting for now.

2. Do you have $40,000+ saved?

Not $20,000. Not “I can borrow some from family.” A real, liquid $40,000–$50,000 safety net. If not, renting while you save is the smarter move.

3. Is your income stable and predictable?

A mortgage doesn’t care if your hours got cut or your freelance client dropped you. If income stability is a question mark, renting keeps you protected.

4. What’s your credit score?

Below 640: Work on this before anything else.

640–680: You can qualify but rates won’t be great.

Above 720: You’re in good shape for Wisconsin’s best mortgage rates.

5. Are you buying because you want to or because you feel pressured?

Social pressure, landlord horror stories, or fear of “missing out” are terrible reasons to take on a 30-year financial commitment.

Wisconsin First-Time Buyer Programs (WHEDA & Grants Explained)

If buying makes sense for your situation, Wisconsin has programs that can seriously reduce your costs:

WHEDA Advantage Loan

Below-market interest rates for first-time buyers. Can save you tens of thousands over the life of your loan.

WHEDA Easy Close DPA

Down payment assistance up to 6% of your loan amount. On a $280,000 home, that’s potentially $16,800 toward your down payment almost free money if you qualify.

Wisconsin HOME Grant

Helps cover closing costs for eligible buyers. Reduces that $8,000–$10,000 closing cost burden significantly.

These programs exist specifically because Wisconsin knows homeownership is hard right now. If you qualify, not using them is leaving real money on the table.

Use a Rent vs Buy Calculator Before You Decide

Numbers on a page are one thing. Your actual numbers are another.

Before making any final decision, run your specific situation through the New York Times Rent vs Buy Calculator it’s the most accurate free tool available and lets you plug in Wisconsin-specific property tax rates, your actual rent, and local appreciation estimates.

What to plug in for Wisconsin:

- Property tax rate: 1.5%–1.85% depending on county

- Home appreciation rate: 2%–4% (conservative Wisconsin estimate)

- Your actual rent vs estimated mortgage payment

The calculator will show you your personal break-even point which is the only number that really matters.

Final Verdict: Should You Rent or Buy in Wisconsin in 2026?

Here’s the honest answer:

Keep renting if:

- You haven’t saved $40,000+ yet

- You might move within 5 years

- Your income isn’t completely stable

- You’re feeling pressured rather than ready

Seriously consider buying if:

- You’re staying in Wisconsin long-term (7+ years)

- You have solid savings and emergency fund

- Your credit score is above 680

- You’ve looked at WHEDA programs and qualify

The biggest mistake people make isn’t choosing the wrong option it’s making the decision based on emotion, social pressure, or incomplete information. Run your real numbers. Know your break-even point. Then decide.

Your Next Step

If you’re getting serious about buying in Wisconsin, understanding the market is step one.

Check what homes in your target area have actually sold for not just their listing price by searching Wisconsin property records here. It’s free and takes less than 5 minutes.

Already own a home in Wisconsin? Make sure you’re not overpaying on taxes. See which property tax exemptions you might be missing in 2026.

FAQ’S

Q1. Is it cheaper to rent or buy a house in Wisconsin in 2026?

In most Wisconsin cities, renting is cheaper monthly, but buying becomes more cost-effective if you stay longer than 5–7 years.

Q2. How much money do I need to buy a house in Wisconsin?

You typically need $40,000–$50,000 for down payment, closing costs, and initial expenses for a median-priced home.

Q3. What credit score is needed to buy a house in Wisconsin?

A minimum of 640 is required for most loans, but 700+ gives you better interest rates and lower monthly payments.

Q4. What is the average rent in Wisconsin in 2026?

Rent ranges from $850 in smaller cities to $1,800 in Madison depending on location and property size.

Q5. When does buying make more sense than renting?

Buying makes more sense if you plan to stay in Wisconsin for at least 5–7 years and have stable income and savings.

Q6. Are there first-time homebuyer programs in Wisconsin?

Yes, programs like WHEDA loans and down payment assistance can reduce upfront costs by $10,000–$20,000.