Wisconsin’s housing market in 2026 looks different from what most people expected a few years ago. Mortgage rates have stayed elevated longer than almost anyone predicted, yet demand in certain Wisconsin metros hasn’t collapsed. It’s just shifted. If you’re thinking about buying or selling property in the state this year, here’s what’s actually happening on the ground and what it means for your decisions.

Quick Answer: Wisconsin’s housing market in 2026 remains stable, with home prices rising modestly in most regions despite elevated mortgage rates. Madison and the Fox Valley continue to outperform the state average, while vacation-home markets such as Door County have cooled.

📌 Key Takeaways

- 🏠 Wisconsin home prices remain stable in 2026.

- 📈 Madison and the Fox Valley continue to outperform most markets.

- 📦 Housing inventory remains tight across much of the state.

- 🤝 Buyers have more negotiating power than in recent years.

- 💰 Higher mortgage rates continue to impact affordability.

- 🌊 Vacation-home markets like Door County have cooled.

- 🏗️ New construction is adding inventory in select areas.

The Big Picture: Stabilizing, Not Crashing

Wisconsin avoided the dramatic price corrections that hit Sun Belt states like Arizona and Florida. Home values across the state are up modestly compared to 2024, somewhere in the 2 to 4 percent range depending on the county. That tells you two things: sellers still have equity and buyers haven’t caught a meaningful break on price.

What changed is the pace. Homes in Milwaukee, Madison, and Green Bay are sitting on the market longer than they were in 2022 or 2023. The frantic multiple-offer chaos has mostly cooled. That doesn’t mean buyers have leverage everywhere. It means the market is acting more like a normal real estate market again, where conditions vary block by block, not just city by city.

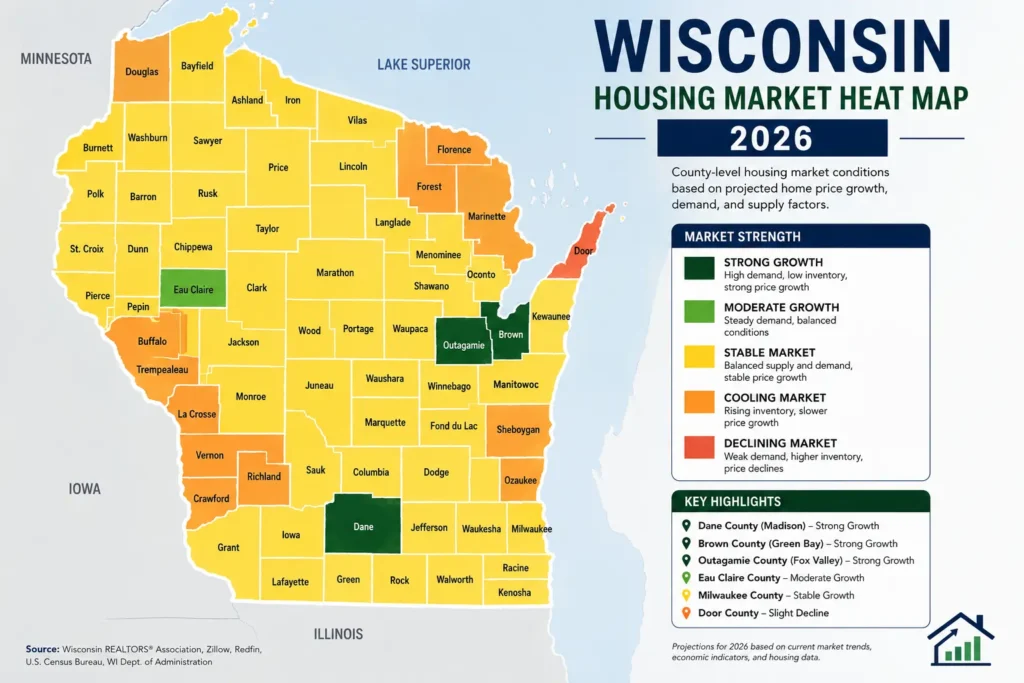

Inventory is the real story. Wisconsin is still undersupplied relative to household formation rates, particularly in the Madison metro and the Fox Valley. New construction hasn’t filled the gap fast enough, partly because builders are dealing with higher financing costs and partly because land close to employment centers is genuinely limited.

Where Values Are Moving: City by City

Madison remains the state’s most competitive market. The university presence, state government jobs, and a growing tech sector keep demand steady regardless of interest rates. The median sale price in Dane County has climbed past $380,000 for single-family homes, and neighborhoods like Fitchburg, Sun Prairie, and Waunakee continue to attract buyers priced out of the city proper.

Milwaukee is a more complicated picture. The East Side, Bay View, and Shorewood have held value well, but the broader Milwaukee County market is uneven. North Shore suburbs like Whitefish Bay and Fox Point attract buyers relocating from Chicago, which has kept prices firm in that corridor. Parts of West Allis and some inner-ring suburbs are seeing slower movement and more price reductions.

Green Bay has been a quiet performer. It’s one of the more affordable mid-size cities in the Midwest, and that affordability has attracted remote workers and younger buyers who don’t need to commute daily. Median prices are well below the state average and days-on-market are still relatively short for a city its size.

Door County and the North Woods lake markets are in a category of their own. Vacation and second-home properties have cooled more than primary residences because they’re more sensitive to consumer confidence and discretionary spending. Waterfront properties are still selling, but the days of anything lakefront moving in a weekend are over.

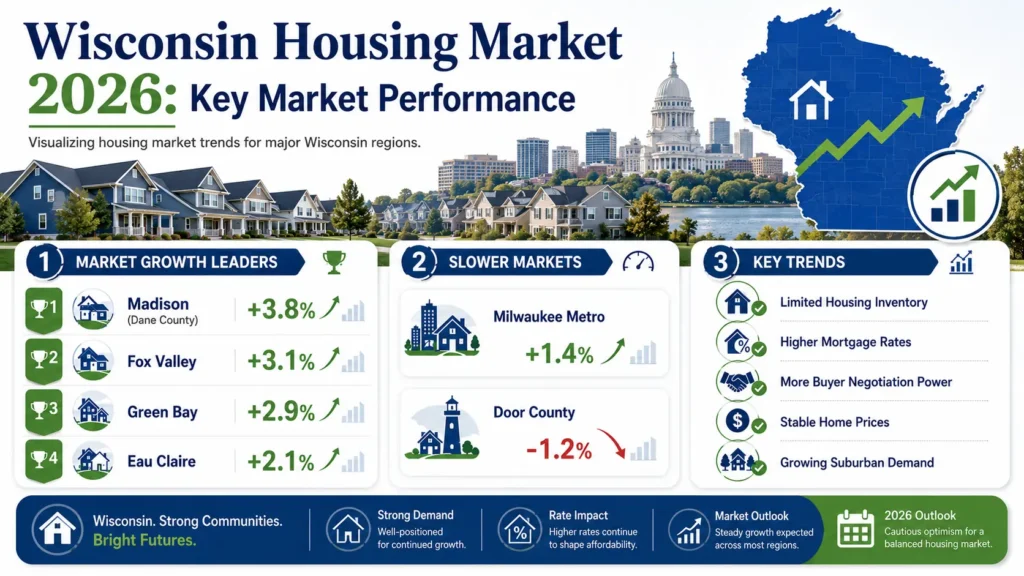

Here’s a snapshot of how the major Wisconsin markets compare heading into mid-2026:

| Market | Median Home Price | Avg. Days on Market | YoY Price Change |

|---|---|---|---|

| Madison (Dane County) | $382,000 | 28 days | +3.8% |

| Milwaukee Metro | $241,000 | 47 days | +1.4% |

| Green Bay | $218,000 | 34 days | +2.9% |

| Eau Claire | $229,000 | 38 days | +2.1% |

| Door County | $398,000 | 74 days | -1.2% |

| Fox Valley (Appleton) | $255,000 | 31 days | +3.1% |

Note: Market figures shown above are illustrative estimates intended to demonstrate general housing market trends and may not reflect current MLS or county-level statistics.

Door County’s slight decline reflects the broader softening in vacation property demand, while Madison and the Fox Valley continue to outperform the state average.

Mortgage Rates and What They’re Doing to Affordability

This is the central tension in the 2026 Wisconsin market. A buyer purchasing a $350,000 home today with 10 percent down is looking at a monthly payment that would have bought a $450,000 home just four years ago. That gap is why so many potential buyers are still sitting on the sidelines.

Consider a real example. A first-time buyer in Sun Prairie found a three-bedroom home listed at $329,000 in early 2026. After getting pre-approved, they discovered their budget had shrunk from what they originally estimated because their debt-to-income ratio was tighter than expected at current rates. They ended up qualifying for $295,000, which put them in a different part of the market entirely. This kind of recalibration is happening constantly right now, and it’s one reason listings in the $280,000 to $320,000 range in Madison’s suburbs are moving faster than anything priced above $380,000.

Rate movement has also changed how sellers behave. Homeowners who locked in 3 percent mortgages in 2021 have almost no financial reason to sell and take on today’s rates. That’s a big reason inventory stays tight even in a slower market.

First-time buyers do have options worth knowing about. WHEDA (Wisconsin Housing and Economic Development Authority) offers down payment assistance and below-market rate loans for qualifying buyers. For buyers in secondary markets like Oshkosh, Racine or Kenosha, these programs can meaningfully close the affordability gap.

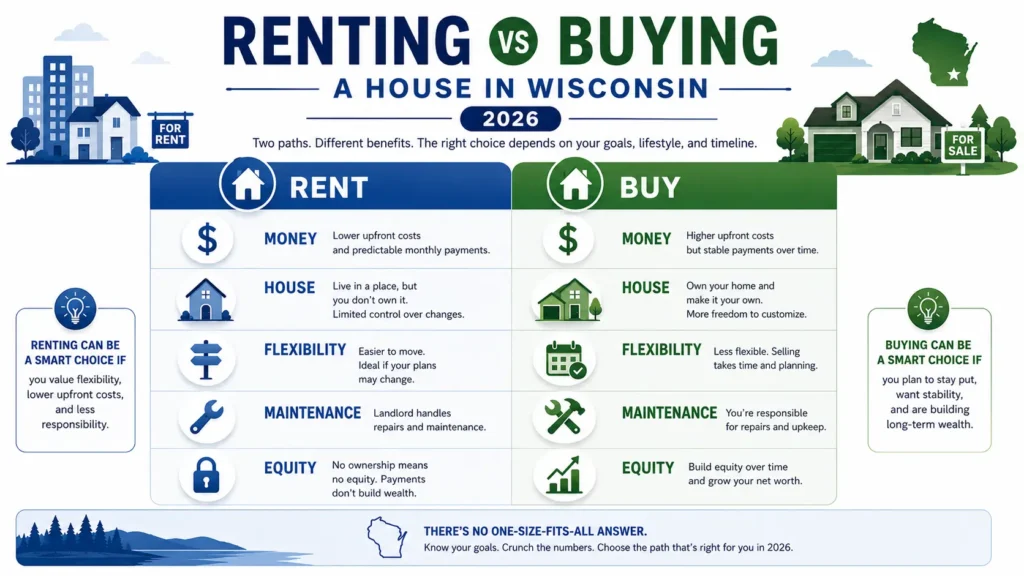

What Sellers Need to Know

The mistake sellers keep making right now is pricing to 2022 comps. That market had conditions that no longer exist: historically low rates, severe inventory shortages, and pandemic-era migration patterns. A home priced at what the neighbor got two years ago will sit, accumulate days-on-market, and eventually sell for less than it would have at a correct price from day one.

Realistic pricing in 2026 means looking at what has actually closed in the last 90 days. Buyers today are more informed and less desperate, so cosmetic issues that used to be overlooked are now being used as negotiating points.

Presentation also matters more than it did a few years ago. Homes that are staged, professionally photographed, and genuinely clean sell faster and closer to asking price than comparable homes that aren’t. Many sellers underinvest in this step because they remember buyers not caring about any of it back in 2021.

What Buyers Need to Know

Negotiating is possible again. In most Wisconsin markets outside the tightest Madison neighborhoods, you can ask for closing cost contributions, inspection contingencies, and reasonable repair credits without losing the deal. That’s a real change from 2021 and 2022 when buyers were waiving everything just to compete.

Before you start seriously looking, get your pre-approval handled. In the current rate environment, surprises can show up between pre-qualification and actual approval, and sellers in competitive situations will prioritize buyers who are clearly ready to close.

Wisconsin homes also have specific things worth watching during inspection:

- Foundation issues related to freeze-thaw cycles, especially in older homes

- Knob-and-tube wiring in pre-war Milwaukee and Madison properties

- Radon levels, particularly in areas with higher geological risk across central and southern Wisconsin

- Roof condition and insulation going into another hard winter

- Basement waterproofing in areas near rivers or with clay-heavy soil

None of these are dealbreakers automatically, but each one costs money, and buyers who skip the inspection are taking on risk they can’t fully see.

Investment Properties and the Rental Market

Wisconsin’s rental market is strong in its major metros. Madison vacancy rates remain very low, driven by university enrollment and a large population of young professionals who aren’t yet in a position to buy. Milwaukee’s rental market has tightened in gentrifying neighborhoods while staying softer in areas with population decline.

For new investors, the math has gotten harder. Cap rates that looked attractive in 2019 don’t work the same way when financing costs have nearly doubled. Anyone entering the rental market now needs to underwrite deals conservatively, meaning realistic vacancy assumptions, genuine maintenance reserves, and no reliance on appreciation to bail out a property that doesn’t cash flow from day one.

Short-term rental markets in Door County, Lake Geneva, and Wisconsin Dells have normalized after the post-pandemic travel surge. Several municipalities have also added regulatory limits on short-term rentals over the past two years. These markets can still work as investment strategies, but pro forma numbers need to reflect 2025 and 2026 occupancy rates, not the outlier years of 2021 and 2022.

What to Watch in the Second Half of 2026

Even a quarter-point reduction in interest rates tends to trigger a wave of buyer activity in Wisconsin, particularly among households who have been waiting on the sidelines. If rates ease before year-end, expect competition to pick up quickly in Madison and along Milwaukee’s North Shore.

New construction in the Fox Valley and Waukesha County is adding inventory that wasn’t there 18 months ago. This gives buyers in those areas more options but also puts mild downward pressure on comparable resale pricing nearby. Sellers in those submarkets should watch new construction pipeline data before setting a list price.

Bottom Line

Wisconsin’s property market in 2026 rewards preparation more than speed. Buyers have more negotiating room than they did in recent years but still face a genuine affordability challenge driven by rates, not prices. Sellers have strong equity positions but can no longer set an ambitious price and expect competing offers to follow.

The people who navigate this market well on both sides are the ones working from current data, not from what they remember the market doing in 2021. Wisconsin’s fundamentals are still solid: stable employment base, reasonable cost of living relative to coastal markets, strong university cities, and real quality of life. The froth is gone and for most people, that’s actually fine.

FAQs

Is Wisconsin a buyer’s market in 2026?

Not entirely. Inventory remains limited in many metro areas, although buyers have gained more negotiating power compared to 2021–2023.

Will Wisconsin home prices fall in 2026?

Most forecasts suggest modest growth rather than significant declines, though local markets vary.

Which Wisconsin cities are growing fastest?

Madison, Appleton, Sun Prairie, and parts of the Fox Valley continue to show strong demand.

Is now a good time to buy property in Wisconsin?

That depends on financing, local inventory, and long-term ownership plans.